Two sets of changes to the Minnesota tax code last year — one aimed at high earners and one at low earners — combined to give DFL tax policy leaders and advocacy groups a national trophy at the start of 2024.

Minnesota is now the state with the nation’s most-progressive tax system in the U.S., as calculated by the left-leaning Institute on Taxation and Economic Policy. Its data-driven assessment looks at the share of state taxes that are borne by various income groups. Progressive is defined not in partisan terms but to describe tax systems that have higher income taxpayers devoting a larger percentage of their incomes to taxes than lower-income taxpayers.

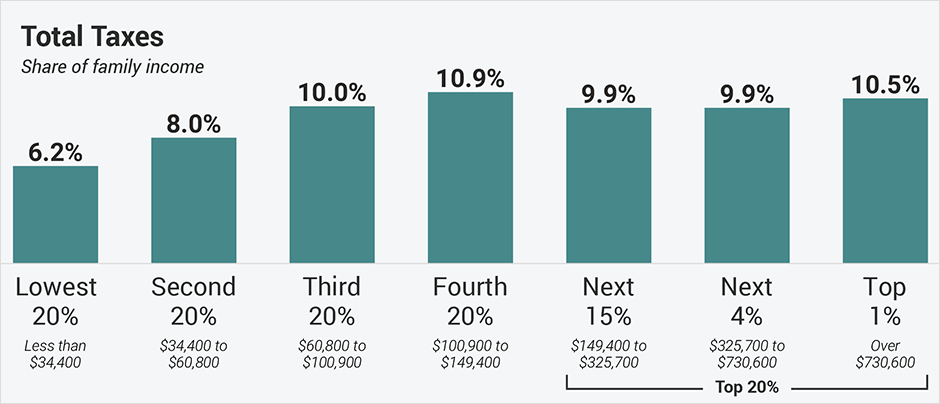

For example, the lowest 20% of Minnesota taxpayers are required to pay 6.2% of income in all state taxes, while the top 1% pays 10.5%. Looking only at the personal income tax, from which the state collects more than half of its revenue, the lowest 20% pays none — either because incomes are too low to require it or because of refundable tax credits people receive, effectively erasing the income tax. The top 1% of Minnesota earners pay 7.5% of income in state income taxes.

[image_credit]Who Pays report/Institute on Taxation and Economic Policy[/image_credit]

“Nationally, comparatively high tax rates on low-income families remain the norm, despite recent steps to lower taxes for this group by bolstering refundable tax credits,” the report states. “Only six states and the District of Columbia now reserve their lowest overall tax rates for low-income families. Those states are Maine, Minnesota, New Jersey, New Mexico, New York, and Vermont.”

The regressivity of most other states — especially those without individual income taxes that rely heavily on sales taxes and other regressive assessments — might set a low bar for reaching No. 1.

[image_credit]Who Pays report/Institute on Taxation and Economic Policy[/image_credit]

What changed? The 2023 taxes omnibus bill adjusted how state taxes impact both the highest earners and the lowest earners. While the House DFL taxes bill would have created a new tax bracket for the highest earners — the so-called 5th tier — the Senate DFL disagreed. A compromise bill eliminated some state tax deductions for the highest earners, exposing more of their income to the current 4th tier. Mark Haveman, the executive director of the business-supported Minnesota Center for Fiscal Excellence, called those changes a backdoor 5th tier, because he notes that it impacts more taxpayers than the House 5th tier proposal would have.

The 2023 session also created a net investment tax assessed on interest, dividends, capital gains, rental and royalty income, and other similar income that exceeds $1 million a year.

On the other end of the income chart, the tax bill made a handful of changes that would reduce taxes paid by lower-income residents. The largest is an increase in the child tax credit, a refundable tax credit that helps families with children, that is worth $1,750 per child. Refundable means that even taxpayers who owe no taxes benefit by getting checks from the state equal to the amount of the credit.

“I think a huge part of this story is tax-credit changes,” said Neva Butkus, a state policy analyst for the tax policy institute. “Minnesota passed the most-extensive, state-level tax credit in the nation. That credit was so targeted to really ensure that lower-and-middle income households are getting additional supports to make ends meet.”

[image_caption]Neva Butkus[/image_caption]

Butkus noted that Minnesota continues to rely on taxes that are regressive — sales taxes and property taxes especially. The treatment of income taxes, however, “counteract the more-regressive aspects of Minnesota’s tax system, things that tend to hit low-and-medium-income families harder.

[image_credit]Who Pays report/Institute on Taxation and Economic Policy[/image_credit]

States at the other end of the scale tend to be states without an income tax or with low-progressivity income tax. Florida is 50th on the list, surpassing Washington state which is now 49th. Seattle Times columnist Danny Westneat jokingly celebrated that the state was no longer the worst, though still of little comfort for low-income people.

Butkus said that even Minnesota and the other top 10 states do not have “a truly progressive system.” The states that are considered to have the most-progressive income taxes still have somewhat flat systems — that is, they take close to the same percentage of income from taxpayers across the income spectrum. The regressive states take higher percentages from lower incomes families than the top earners.

Butkus said sales taxes and property taxes have a place in state tax codes because they help stabilize tax collections through economic downturns.

[image_credit]Who Pays report/Institute on Taxation and Economic Policy[/image_credit]

The Minnesota Department of Revenue conducts what it calls a tax incidence report on the state tax system that will include the changes made last May. That report conducts an analysis similar to the institute’s study to show how state taxes are distributed across income groups. It is expected to be released March 1.

While not part of the Institute on Taxation and Economic Policy study, which looked at tax impacts on individuals and families, Minnesota also climbed in one other tax measure: corporate taxation. The conservative Tax Foundation reports that of the 44 states with a corporate income tax, Minnesota’s 9.8% top marginal rate is the highest. But it claimed the superlative not due to any legislative changes but only after a pandemic-era surcharge in New Jersey expired.

[image_credit]Who Pays report/Institute on Taxation and Economic Policy[/image_credit]

“Minnesota has among the worst pre-tax racial income inequalities in the nation. Minnesota’s progressive income tax system narrows this gap somewhat, but we should do more to unleash the power of the tax code to advance racial equity,” the report states.

The budget project added that fairness is only one measure for a tax system, with adequacy being another. That is, does it raise enough money to pay for services? “Minnesota has taken an approach to tax policy that has paid off for the residents of our state, and there is still work to do to create a more equitable tax system that sustainably funds the public services Minnesotans want and count on.

“Minnesota has taken an approach to tax policy that has paid off for the residents of our state, and there is still work to do to create a more equitable tax system that sustainably funds the public services Minnesotans want and count on,” wrote the budget project.

Gov. Tim Walz and DFL leaders celebrated the 2023 budget, along with other legislation, as transformative and historic. The current budget is 40% higher than the previous two-year budget. And while some of that is one-time spending, fueled by a record $17.5 billion surplus, the next budget will be significantly higher than the 2021-22 budget. The tax increases noted above are permanent.

The state economic and revenue forecast in December reported that the state will have just $2.4 billion left over when the current, $71 million budget runs its course on July 1, 2025. Because some of the spending does not carry over to the 2025-26 budget, the state would need $66.2 billion to cover ongoing costs. But current taxes are only expected to raise $64 billion over that same time, leaving what budget managers called a “structural imbalance.”

Both Walz and DFL legislative leaders urged restrained expectations for budget and taxes for the session that convenes Feb. 12.

“I’ll tell the Legislature, we did a lot of great work last year. It’s time to implement that,” Walz said after seeing the forecast. “It will have a positive impact on workforce development, on housing, on the environment. But we need to be measured, we need to be cautious. This is not the year.

[cms_ad:x104]

“If we’re cautious on this we balance out in the out years,” Walz said.

Minnesota Management and Budget must produce a new economic and revenue forecast later in February, and it is that forecast — expected the last week of the month — that will drive any supplemental budget and tax bills.